How might the sanctions of the EU as a response to the Russian invasion in Ukraine affect international trade, GDP and inflation in the EU and in Austria in particular?

While trade between the EU and Russia had been growing following the Partnership and Cooperation Agreement (PCA) in 1997 and Russia’s accession to the WTO, this trend was reversed from 2014 onwards, after restrictive measures were imposed by the EU as a response to Russia’s annexation of Crimea. As a consequence, Russia started diversifying its imports and cooperating tighter with other trading partners such as China. The Federation’s countermeasures have especially affected the EU agri-food industry, which saw its exports plummet.

Just over one third of this country’s overall exports and imports flowed in and out of the European Union, making it Russia’s biggest trading partner. Furthermore, the EU is Russia’s largest foreign direct investment source, its stock lay at €311.4 billion in 2019. [1]

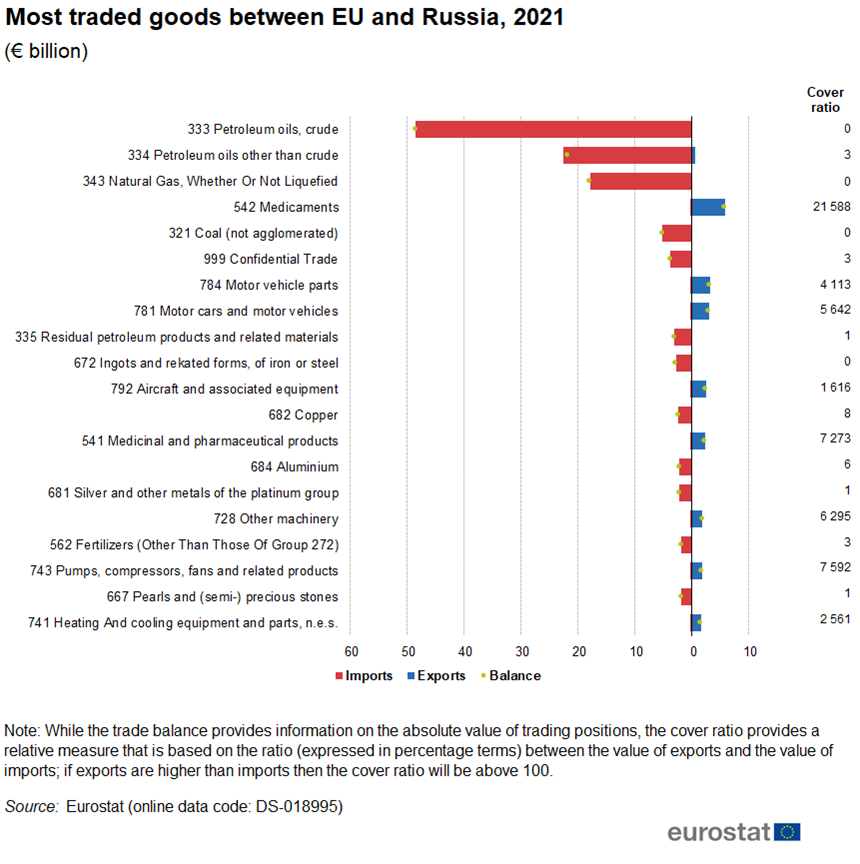

Mineral fuels are not only the Union’s main import goods from Russia, but also constitute the most vulnerable sector for both trading partners. On the one hand, the EU depends heavily on Russian oil and gas imports (roughly 27% of all its imports for oil and 41% for gas)[2], and on the other hand, the Russian current account’s surplus in the past years has originated from the significant revenues this sector generates.

Within the manufacturing sector, the EU’s most important export products to Russia are medicaments and pharmaceutical products, cars and car parts as well as semi-conductors.[3] The Federation relies on high-tech imports from western countries generally, as these are needed for the modernization of its industries and thus crucial for its long-term growth.

Looking at the trade relation of Austria and Russia in particular, Austrian exports amounted to 2,1 billion EUR and its imports to 3,29 billion EUR in 2018[4]. The structure of these does not differ significantly from the European average – Austria exports machinery and technological equipment and pharmaceuticals, while it imports mostly oil, gas and metals. Before 2014, agri-food products played a large role as well.

In the last week of February 2022, the EU has agreed, with unprecedented swiftness and scale, on a large number of restrictive measures in response to Russia’s invasion in Ukraine. Among them are a tightening of the existing trade restrictions on dual-use goods as well as new ones concerning the following sectors: high-tech, oil refinery, aerospace and aircraft. These cover microprocessors and semiconductors, two important Austrian export products. As of today, it is certain that the sanctions will negatively affect exports of Austria and the EU generally, decreasing their trade volume with Russia. Yet the consequences of not only the trade-related measures, but also the sanctions package and the armed conflict overall may not yet be quantified. These will depend on a variety of factors, most notably the type and scope of Russian countermeasures. In the worst-case scenario, these would include an interruption of oil and gas deliveries, which could precipitate unprecedented inflationary pressure in Europe and a exasperate the already commencing recession in Russia.

Further Source:

[1] https://ec.europa.eu/trade/policy/countries-and-regions/countries/russia/

[2] https://ec.europa.eu/eurostat/cache/infographs/energy/bloc-2c.html

[3] https://ec.europa.eu/eurostat/statistics-explained/images/e/e7/Most_traded_goods_between_EU_and_Russia%2C_2021.png

[4] https://www.wko.at/service/aussenwirtschaft/Advantage-Austria—Lukavsky—Russian-Austrian-Economic-Rel.pdf

{kind=link}